This blog was published in full on tradebetablog. What follows is an abridged version of the original piece.

Leaving the EU means the British government will either have to convert the EU’s free trade agreements with other countries into UK deals, or risk losing them. Academics at Sussex University say there are over 60 other countries. The UK government says there are over 100. It depends on what kind of agreement is counted.

Even then, the “rolled over” free trade agreements could be less valuable to the UK outside the EU than inside, unless talks can be set up with all three parties leading to something called “diagonal cumulation of rules of origin”.

Much of the complexity is shown in a paper (pdf) by Michael Gasiorek and Peter Holmes of Sussex University and published by the UK Trade Policy Observatory (UKTPO). They say something that few had considered: that what appears to be a set of bilateral talks will turn into a threesome — the EU will be involved too.

What I am going to do here is to dip into the EU-South Korea free trade agreement — and I really mean “dip in” because it’s over 1,400 pages long — to highlight a few issues that will come up when trying to “roll over” these agreements.

Possible to do; impossible to do quickly

The bottom line. Is grandfathering difficult or impossible? No, for the most part, it shouldn’t be. But even where it’s relatively straightforward, the task is time-consuming. There’s a lot to copy, adjust and check. If there were only one agreement to deal with, it could be completed quite quickly. But the number of negotiations the UK will be involved in for Brexit is huge.

Then there are the more complex areas such as “tariff quotas”, agricultural “safeguards” (there aren’t many in the EU-S.Korea agreement but there are a lot more in the agreement with Canada) and “rules of origin”. It becomes even more complicated if the other countries want to negotiate additional adjustments.

Grandfathering: more than CTRL+C, CTRL+V

You don’t have to go very far into the text to see that there are references to the EU which will have to be replaced by the UK’s equivalents.

Numerous references to EU procedures and regulations will also have to be changed.

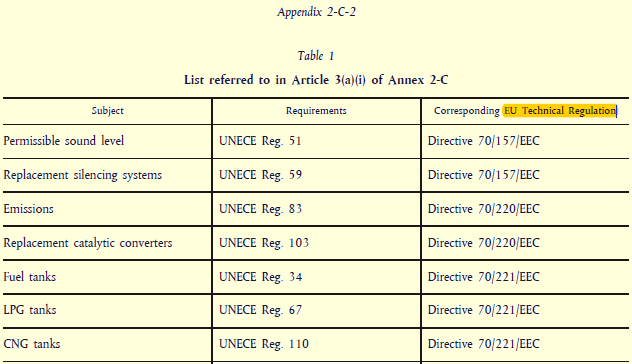

The endless lists of regulations will have to be replaced with UK versions. This is just a small part of a long table of regulations for vehicles.

All of this is also bound up in how the UK sorts out its own post-Brexit arrangements.

And provisions such as this would have to go:

And then there are services. The EU-S.Korea agreement has long lists describing where their services markets are opened up to each other (pages 1165-1250 for the EU’s commitments). Much can be copied for the UK. There are also lots of provisions which don’t apply to the UK and will have to be removed, and a lot that refer to the EU as a whole, which will have to be changed.

This is what the agreement says for mining and quarrying services. It’s complicated, technical stuff, but even if we don’t understand it fully, at the very least “5% of the European Union’s oil or natural gas imports” will have to be changed to “the United Kingdom’s”. You have to be an expert in the field to know if that “5%” will stay unchallenged.

“EU: Unbound for juridical persons controlled […] by natural or juridical persons of a non-European Union country which accounts for more than 5 % of the European Union’s oil or natural gas imports. Unbound for direct branching (incorporation is required). Unbound for extraction of crude petroleum and natural gas”

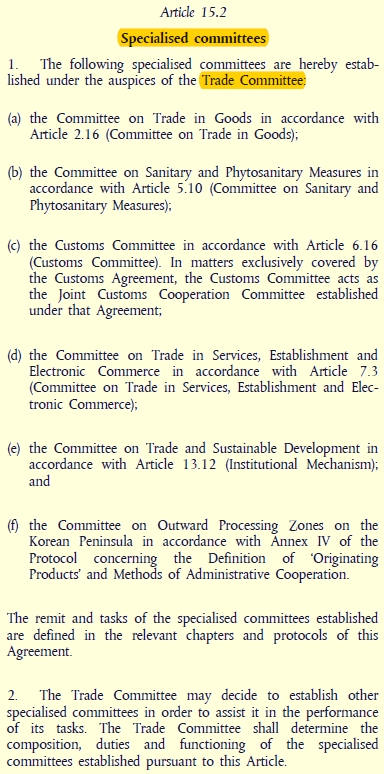

Finally there are institutional arrangements, everything from committees and working groups to arbitration procedures, which will have to be set up for the new bilateral relationship. Article 15 creates a “Trade Committee”, which meets annually, plus at least six “specialised” committees and at least seven working groups:

The agreement includes procedures for settling disputes, including the creation of arbitration panels and references to international law including the Vienna Convention on the Law of Treaties and World Trade Organization dispute rulings. The procedure is similar to the WTO’s and adapting it for the UK would be relatively simple.

Photocopier? Or negotiating table?

Where negotiations will be needed is on market access, particularly for goods, but only on some parts. For goods, the EU-S.Korea agreement lists tariffs on around 900 pages. They could be run through the photocopier — except that S.Korea is reported to be one of the countries that might seek unspecified concessions in order to address its trade deficit with the UK. For a country which prioritises exporting goods, this is a first order issue.

In many cases, tariffs are not scrapped from the start: they are phased out over different periods depending on the product, from immediate (most products) to 21 years and in some cases tariffs are never eliminated (“staging category E”). So the UK would be stepping into an appropriate phase of the reductions (unless “rolling over” took more than two decades!)

What most people forget is the EU’s free trade agreements include tariff quotas as well. That’s where limited quantities of imports are allowed in duty-free or at lower than normal rates, also known as tariff-rate quotas or TRQs. And it’s where negotiations will probably be needed.

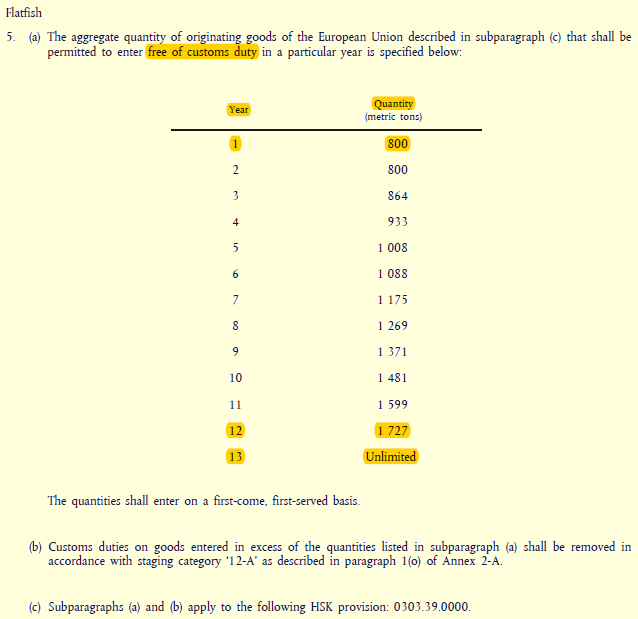

The EU-S.Korea agreement has a few, mainly on the Korean side. Here’s one for flatfish where the duty-free allowance increases from 800 tonnes in year 1 to duty-free for all imports from year 13.

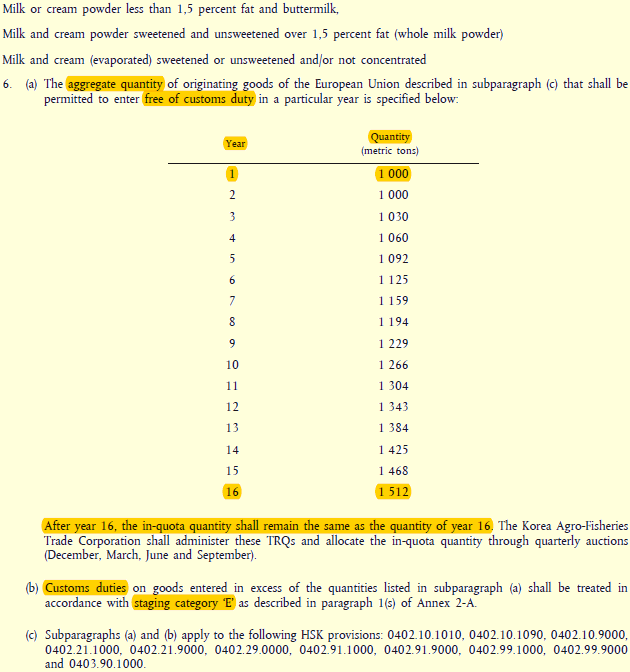

Here’s another on various types of milk and cream. This time the duty-free allowance remains indefinitely at 1,512 tonnes after year 16 (“staging category E”), meaning quantities outside the quota will be charged import duty, which is 89% or 176% depending on the product. (The tariff rates are on page L127/102 of the EU’s version of the text (pdf).)

What will the UK’s share of that 1,000–1,512 tonnes be? The answer is likely to come from talks among all three sides: the UK, EU and S.Korea.

Safeguards

One type of tariff barrier that has received little attention is “safeguards”. These are temporary increases in import duty to protect producers from import surges or falling prices, the kind of raised duty the US recently imposed on washing machines and solar panels.

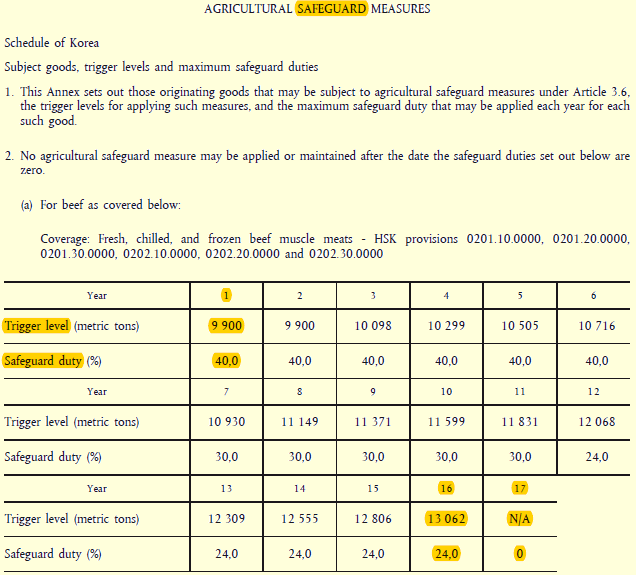

For agricultural products and in bilateral trade agreements the rules are not quite the same as for industrial goods. Here, S.Korea has secured the right to impose an additional duty on beef imports of up to 40% for the first six years, the ceiling declining to zero after 17 years, if the “trigger level” specified is reached.

S.Korea has the right to use safeguard duties on pork, apples, malt and malting barley, potato starch, ginseng, sugar, alcohol, and dextrins. For beef the right to impose a safeguard duty expires after 16 years. For pork it’s 11 years, for apples 24 years, and for other products somewhere in between.

The trigger volumes were for the whole of the EU-28. Copying the same trigger level for imports from the UK alone would not make sense for S.Korea. To do so would double the size of the import surge before Seoul could react. That means these volumes would be split between the UK and EU, requiring negotiations between all three sides.

The dreaded rules of origin

To qualify for lower duty or duty free access to the EU market, or for recognition of standards under the agreement, a product has to be shown to have been made in S.Korea. The same goes for EU products entering S.Korea, and for UK products under a future UK-S.Korea deal.

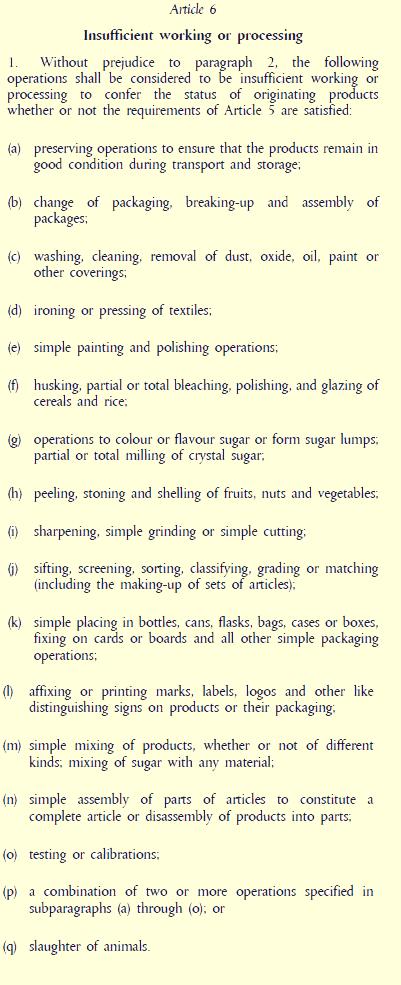

Anyone who has looked at these “rules of origin” knows they can be pretty complicated, to the extent that lower tariffs are not always worth the additional red tape. The criteria start with general rules on what qualifies and what proof is needed, covering 8 pages (1346–1354) in the EU-S.Korea agreement. For example, Article 6 lists 17 operations that cannot be cited — “sharpening, simple grinding or cutting” is not enough (item (i)). Nor is it enough if two ingredients from elsewhere are simply mixed together in the EU — they cannot be said to be “made in the EU” (item (m)):

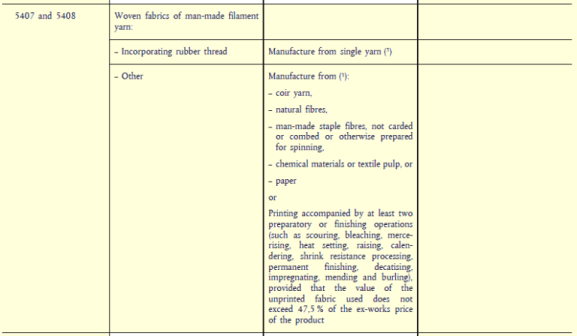

But that’s just the start. A further 57 pages have tables of excruciating detail — like this on what is required for two types of “woven fabrics of man-made-filament yarn” to qualify with the right origin:

(Note that in that last paragraph, the product can qualify even if the value of the unprinted fabric exceeds 47.5%, so long as the fabric itself is also of local origin.)

Could these rules of origin just be run through the photocopier? Maybe. But remember right now exports from the UK to S.Korea only have to qualify as “made in the EU”, meaning components could be sourced anywhere in the 28 countries. A post-Brexit UK-S.Korea free trade agreement would only deal with products “made in the UK”.

In other words, from the point of view of qualifying products, a future UK-S.Korea agreement will be much less valuable for the UK than the present EU-S.Korea agreement.

Finally, how well does EU-S.Korea represent other EU free trade agreements? It depends. No two agreements are the same, but they can be similar. The Korean agreement is partly similar to the Canadian one but also has significant differences.

Norway and Switzerland are important trading partners of the UK. One of the most complicated agreements for the UK to grandfather is the one with Norway, Iceland and Liechtenstein — the European Free Trade Association (EFTA) countries, which form the European Economic Area (EEA) with the EU.

As for Switzerland, its arrangement with the EU is through bilateral agreements. Here, the official list (pdf) — containing only the names of the agreements — runs to 28 pages!

One comment