In this ‘Trade 101’ piece, Tarlochan Lall explains in detail what leaving the European Union’s Value-Added Tax area means for consumers – including for online purchases.

This is the second part of a two-part series on VAT post-Brexit. Part 1 dealt with business to business supplies. This part deals with supplies to consumers (“C”) (B2C). B2C supplies have an impact on both businesses and consumers.

This article first outlines the current system, before examining the consequences of the UK leaving the VAT area, including the implications of a hard Irish border. It then discusses some of the post-Brexit options.

In summary:

- Consumers will have to become aware of duty free allowances on goods brought into the UK from EU states. They will be required to pay UK VAT on any goods above a given monetary threshold.

- Internet sales will be strongly affected: postal purchases would be subject to UK VAT when above a given monetary

- Neither the EU’s customs union nor the European Economic Area cover VAT. So remaining in either or both would not solve the questions surrounding VAT post-Brexit.

- While the UK could seek to replicate EU VAT rules, the government has indicated that it will not allow the UK to be bound by European Court of Justice rulings, a requirement for the UK to remain in the EU VAT area. This creates uncertainty for businesses.

- In Northern Ireland, differences in VAT duty rates post Brexit mean it would be very difficult to prevent border controls.

*****

It is a basic principle of VAT that it is intended to be a tax on final consumption. Whether VAT is chargeable and how much of its burden can be passed to the consumer directly affects the price payable by the consumer, which has direct implications for sales. There are separate rules for goods and services.

Businesses supplying to consumers effectively act as unpaid tax collectors: they collect the amount charged to the consumer and then account for that amount to HMRC each quarter. Consequently they bear the risks of getting the law wrong: if they do not charge VAT where they should, they will be assessed for the amount due, and (in most cases) will be unable to recover that amount from the consumer.

How VAT currently works on business to consumer goods and services moving across borders

B2C supplies of goods

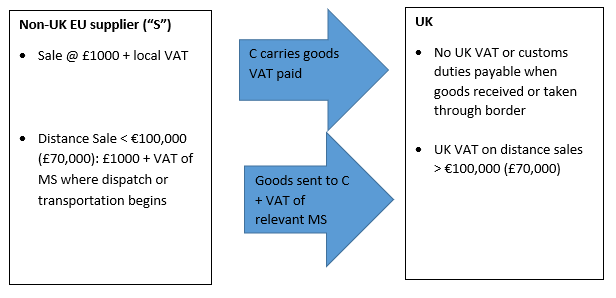

Figure 1 – Movement of goods within the EU

The general scheme for B2C goods moving across borders is that S charges VAT in the country where the goods are located when supplied. That is normally the place where S is established, assuming the good are handed over by S to C. C, travelling within the EU, can move the goods freely without having to pay VAT or customs duties. So if C, a UK resident, buys an expensive item of jewellery in Paris, he will pay French VAT, and will pay nothing when carrying it back into the UK (even if the UK rate is higher).

The position becomes more complicated where goods are sent to C by some method.

Firstly where S is established in the EU and the goods are moved to the UK before sale or are in the UK when sold, S must register for VAT and charge UK VAT. So a French jeweller travels to London with a selection of jewellery and makes a sale of one of her pieces, the jeweller will need to register for UK VAT and UK VAT will need to be charged.

Secondly, if S arranges delivery from outside the UK (for example, where a UK resident orders an item of jewellery from a shop in Paris), such transactions are known as distance sales. As shown in figure 1, where a supplier in one EU member state dispatches goods from outside the UK, VAT of the country of dispatch applies. So, if a French supplier arranges for goods to be sent to a customer in the UK and the supplier’s sales in a calendar year are below €100,000, the supplier must charge French VAT. But once the sales exceed €100,000, the French supplier must register for VAT in the UK and charge UK VAT.

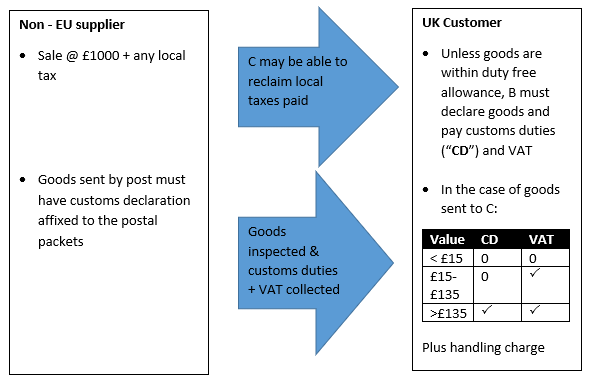

Figure 2 – Goods coming into the EU

Where C brings goods into the UK from outside the EU, C must declare them if their value exceeds the duty free allowance and pay applicable customs and excise duties and VAT. Duty free allowances for alcohol and tobacco are well known. In the case of other goods, currently where goods worth over £390 are brought into the UK, they are liable to customs duties and VAT unless a lower rate is applicable, and must be declared. There is a lower allowance of £270 for those coming into the UK by private plane or boat as they are not treated as having travelled by “air or sea”. That lower allowance would apply to Channel Tunnel travellers unless the law is changed.

The continuing growth of e-commerce means that goods are more likely to be sent to C by post or courier. Where goods are imported by C into the UK from outside the EU and they are sent by post, VAT applies to goods worth more than £15 (goods below benefit from what is known as “low value consignment relief” (LVCR) – there is an exception to this rule for exports from the Channel Islands, in order to stop the widespread use of LVCR to enable the VAT free supply of CDs into the UK from the Islands) and customs duties apply to goods worth more than £135. The goods must travel with a customs declaration. If it is missing, C can be required to provide one and failure to do so may result in the goods being sent back or disposed of. The postal operator or courier requires the VAT and customs duties to be paid before delivery and they add their handling charge.

Increasing amounts of sales are over online market places and the goods are already in the UK to ensure prompt delivery to customers. Sales by overseas sellers of goods already in the UK are subject to UK VAT. Non-EU sellers must register for VAT and cannot take advantage of the registration thresholds for EU distance sales, so they must register no matter how small the total sales.

In reality, however, many Non-EU sellers do not register for VAT. Widespread non-compliance and fraud has led to rules being recently introduced making online marketplace operators, such as Amazon, liable for the unpaid VAT where they know or should have known that the seller has not registered for VAT and they do not stop the seller using their online market place. Those rules also seek to remove the competitive advantage overseas suppliers have over UK suppliers of selling goods at lower prices because they think they can sell without paying VAT.

Where C buys goods in the EU but then takes them out of the EU (for example, where an American buys jewellery in London and takes it back to her home in Houston), VAT paid can be reclaimed on leaving the UK by making a claim at the port of departure. Where goods are sent out of the UK by post, again a customs declaration must be sent with it.

B2C supplies of services

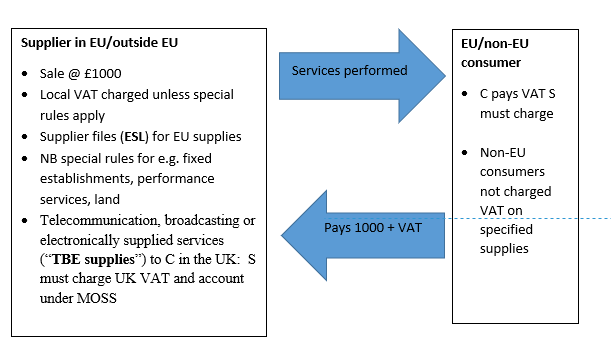

Figure 3 – Supplies of services to EU and non-EU customers

The starting point for B2C supplies of services is that they are supplied where the supplier is established and the supplier charges local VAT. This is the opposite of the position for B2B supplies. A UK supplier charges UK VAT; a EU supplier charges VAT in their member state; and a non-EU supplier does not charge UK VAT but may charge whatever sales tax is due in its country.

However, S must consider whether it has a “fixed establishment” where, the services are regarded as performed in the country where C is. For example although established outside the UK, the performance of services by S in the UK may create a UK fixed establishment such that S must register for VAT and charge UK VAT. For example, if a foreign firm S rents a UK office and meets its clients there, it may well be regarded as having a fixed establishment in the UK and to be liable to pay UK VAT on supplies made from that office. So UK suppliers need to assess whether they have an overseas fixed establishment where they supply services to overseas customers. Within the EU the aim is to have harmonised rules on what counts as a fixed establishment although the practices of individual member states can vary. Outside the EU, the rules of the relevant countries must be considered.

Where actual performance takes place in a country other than where the supplier is established, or has a fixed establishment, different rules apply.

There are rules for certain categories of services where the service is treated as supplied in a different place to that where the supplier is established. For example, certain land related services (such as carrying out a survey of a building or acting as a conveyancer) are treated as made where the land is situated (“land related supplies”). Certain categories of supplies are treated as made where they are actually performed, for example cultural, artistic, sporting, scientific, educational, catering and entertainment services, and certain transport services (“performance supplies”).

There are special rules for TBE supplies. They are treated as made where the recipient belongs. This means that the supplier may have to register and account for VAT in a number of countries where they have customers. To ease administration and avoid the need for multiple VAT registrations, a mechanism known as the mini-one-stop-shop (“MOSS”) was created. MOSS essentially allows the supplier to register in one EU member state, e.g. UK, and account for VAT due to each of the EU countries where they have customers in the UK. MOSS was a trial system for such services and is intended to be rolled out more widely in the EU. A non-EU supplier of TBE supplies can choose which EU country they register in.

There are further special rules for certain categories of services supplied to non-EU customers. They are treated as made where the recipient is based so they are outside the scope of UK VAT. The supplier does not charge the customer any VAT. The categories of supplies include specified intellectual property, advertising, services of professionals such as consultants, lawyers and accountants, financial and insurance services, supplies of staff and hire of goods (“specified supplies”).

Where a supplier established outside the EU makes supplies to customers in the EU and the services consist of performance or land related supplies, or TBE supplies, the overseas supplier may have to register for VAT in the country concerned and has to account for VAT.

For example, in the case of TBE supplies, the supplier can choose which country they have their MOSS registration. There are two MOSS registration schemes, one for EU established businesses and another for non-EU businesses. In every case, a supplier based outside the EU must consider whether they have a fixed establishment in another country, and if so, the fixed establishment must normally be registered for VAT in that country. This is also the case for TBE supplies, when MOSS cannot be used.

The impact of Brexit

On leaving the EU, the position of UK residents buying goods in the EU would be very different. Currently, they pay VAT in the country where they purchase the goods but can then move the goods freely from one EU state to another and bring them into the UK without customs duties or VAT. After Brexit, they will have to be conscious of duty free allowances. If the goods brought into the UK exceed the duty free allowance, they will have to be declared and VAT and customs duties paid when coming through the port. However, they will also be entitled to a refund on VAT paid in the EU (if they can be bothered with the necessary paperwork).

In view of increasing e-commerce, the biggest impact on consumers would be on postal purchases from the EU, which will become subject to UK VAT and customs duties where they exceed the VAT and duty thresholds. However, the Government has announced in its “no deal” notice on VAT that, on a “no deal”, the rules will change for all postal purchases from overseas: LVCR will be abolished completely but any foreign seller who registers for UK VAT will be able to certify, for packets worth up to £135, that it will account for VAT on that sale, and carriers of certified packets will not be required to pay VAT on import. Carriers of packets worth over £135, and non-certified packets, will however have to pay VAT on delivery. In addition, there will be handling charges to pay.

EU suppliers would be exporting out of the EU so they will not have to charge local VAT or register for VAT in the UK under distance selling rules (unless they wanted to benefit from the UK scheme for imports worth less than £135). The VAT collection burden would shift to postal operators.

Similarly, UK suppliers sending goods to EU customers would not have to register in the customers’ country under distance selling rules. But the customer would be importing goods from outside the EU and would be liable for customs duties and VAT in their country on importation – and there will be no equivalent to the UK’s scheme for imports worth less than £135.

Where EU suppliers to UK customers source their goods in the UK for delivery to their customers, they would be liable to register for UK VAT and charge their customers UK VAT as they do now. In addition to shifting the VAT burden to online market place operators as mentioned above, the UK is considering introducing a mechanism for ‘split payments’ forcing payment service providers involved in the supply chain to strip out the VAT and pay that to HMRC. Although the EU is also considering such a mechanism, it will require a change in EU law. Post Brexit, the UK would not have to wait for the EU law to be changed. UK suppliers sourcing goods in the country of their customer will have to consider local registration and VAT requirements as they do now.

In the case of TBE supplies to consumers, a UK supplier could use the MOSS registration scheme, but a new MOSS registration would be needed in another EU state rather than the business being able to retain a UK MOSS registration. The UK business would be within the MOSS scheme for non-EU businesses rather than the one for EU businesses. Simplifications introduced for small businesses using MOSS from 2018 are not available to non-EU businesses, so small UK business will not be able to rely on those simplifications from 2021 – assuming there is a transitional period..

Where B2C supplies of goods are made and the movement of goods begins in an EU member state, once again the business may require a VAT registration in those EU countries. Again this is not fundamentally different from the position now.

Where a UK business makes performance or land related supplies in the EU, the UK business would require VAT registrations in each country where such supplies are made. Although the position is not fundamentally different from the position now, a UK business may still remain in the EU VAT system although its main establishment would be in the UK.

Irish border

Avoiding a customs border between the Ireland and Northern Ireland is a hot topic as it is also political. The UK and the EU cannot agree how to deal with this problem.

Politics aside, a border between Northern Ireland and Ireland will result in goods movements being subject to customs procedures and the payment of customs duties. The VAT cost must not be underestimated as the VAT rate is usually higher than customs duties. Keeping Northern Ireland in the customs union would deal with customs duties but not VAT unless rules are introduced to keep Northern Ireland in the VAT area as well, which will not happen unless the UK as a whole remains within the VAT area.

Different issues would arise for consumers. Most obviously, since Ireland’s standard rate of VAT is 23% against 20% in the UK, there is an incentive for Irish consumers to buy in Northern Ireland and take goods back. Currently there are no limits on such cross border trade. Post Brexit Irish consumers would be subject to applicable duty free limits. If the UK starts extending reduced or zero rates to certain products, which it would be free to do, incentives for cross border trade would increase, which it would be very difficult to prevent without border controls.

There may be potential for structuring cross border supplies of services, especially specified supplies. For example such services supplied from Ireland to say consumers in Northern Ireland would be free of VAT assuming the Irish supplier does not have any fixed establishment in Northern Ireland. The UK will need to decide how to treat such supplies to UK consumers. Unless the UK imposes VAT on such services, they could also be supplied tax free, again assuming the UK supplier has no fixed establishment outside the UK.

Options post Brexit

Assuming the transitional period is adopted, essentially until December 2020, the current treatment described above will continue. It would allow businesses time to prepare for changes that would take place on 1 January 2021. It is possible that the temporary solution for the Irish border proposed by the UK Government would extend the preparation period by a year or more.

There are separate rules for customs duties and VAT. Although VAT is collected as a customs duty as shown above, for example there are different thresholds for VAT.

Customs union

The EU’s customs union allows goods to move freely without the payment of customs duties and compliance with customs procedures. The UK remaining in the customs union would mean that consumers bringing goods with them from the EU would not have to pay customs duties. However the Government will need to decide what to do about VAT.

That is also the case for goods sent to the consumer. Where goods are sent to a UK consumer from an EU state, the supplier will be exporting them out of the EU for VAT purposes and would not charge VAT. The consumer would have to pay VAT on goods above £15 and the postal operator would have to collect and account for the VAT.

VAT area

The VAT area generally consists of countries which adopt common EU rules on VAT. Remaining in the EU VAT area as well as the Customs union would allow the existing system described above to continue. However, it would require the UK to follow EU law on VAT and be bound by the decisions of the European Court of Justice, which is one of the UKs’ red lines.

The UK may create a parallel VAT regime. That will mean existing VAT rules being replaced by new rules seeking to do what the existing rules do. There will remain the question whether the new parallel rules achieve the same result as current law or whether they involve traps for business and consumers. In time, the UK VAT law, freed form the CJEU law, may diverge as UK courts interpret rules in their own way.

European Economic Area

The EEA exists under a 1993 agreement between the EU, its member states and States of the European Free Trade Area (“EFTA”). The agreement applies to Iceland, Lichtenstein and Norway and the members of the EU, but not Switzerland.

There are no customs duties on goods originating in the member states of the EEA except as provided in the EEA Agreement. Therefore, some customs duties may apply.

The EEA Agreement does not cover the EU’s customs union or rules on tax. The EU VAT rules do not apply.

The EEA would give some benefits of the customs union, but none of the benefits of the VAT area unless the UK creates rules to mirror the current regimes. As said, the new UK rules would have to be tested to assess whether they do successfully replicate the current regime.

The July 2018 White Paper

The white paper on ‘The Future Relationship between the United Kingdom and the European Union’ published on 12 July declares that the UK is leaving the Single Market and the customs union.

The “core” proposal in the white paper is “the establishment by the UK and EU of a free trade area for goods”. Services, which form circa 80% of the UK economy would be dealt with under

“… new arrangements for services and digital, recognising that the UK and EU will not have current levels of access to each other’s markets in the future.”

The UK is proposing a new arrangement rather than adopting an existing known model, such as the EEA. The Taxation (Cross border Trade) Act 2018 provides for the creation of a new customs system. Amendments made to the draft bill in July sought to ensure that the UK will be leaving the VAT area.

The model the UK is seeking would apply to goods, small parcels and to individuals travelling goods, (including alcohol and tobacco) for personal use.

The EU’s formal response to the white paper is awaited although initial indications are that they have a number of questions over the UK’s proposal.

Planning for change

The description above is an outline and seeks to give an overview. The rules have to be tested in any given situation. The complexity is self-evident.

The rules have developed over more than forty years and businesses have become familiar with them although many issues and disputes arise. Even if the UK seeks to replicate the existing rules, businesses and consumers would have to cope with new interpretations of them by UK courts unconstrained by the European Court of Justice. Although the EU has sought to create a harmonised system, many disputes have arisen in the past where the UK’s style of implementing EU law has not achieved what the EU law required. Businesses will, therefore have to come to terms with new rules and assess whether their rights and obligations remain the same. There will be inevitably be additional burdens for business in coping with this change.

All the attention has been on customs duties and the movement of goods in the Brexit debate. Not enough attention is being given to VAT rules or the implications for services. Both of those areas are large in scale in the UK economy. The many businesses affected by them will have to assess the impact of Brexit and plan for change.

Tarlochan Lall is a barrister at Monckton Chambers.

He thanks George Peretz QC for his comments.